P&C Intelligent Underwriting Workbench Applications 2023 Vendor Assessment

IDC OPINION The commercial property and casualty (P&C) insurance outlook faces challenges from economic uncertainties, mounting regulatory compliance complexity, ever-demanding digital customer expectations, structural changes in the risk landscape, and rising claims inflation. While recent years saw strong financial performance driven by risk-adjusted rate hardening, commercial carriers are now confronted with slowing rate growth and uncertainty in pricing adequacy. Mounting competition from distributors, decarbonization pressure, and the need to address emerging risks such as natural catastrophes and cyberthreats add to the hurdles. Bridging the protection gap is vital to retain relevance. Moreover, tightening capacity in traditional reinsurance and alternative capital markets further complicates matters. To thrive, carriers must adapt underwriting practices, invest in technology, and develop innovative solutions to navigate this inflection point successfully.

IDC observed a growing trend in the commercial property & casualty (P&C) insurance industry in which insurers are increasingly investing in digitalization and automation to modernize their core business functions, particularly in underwriting and policy administration. The underwriting process in commercial P&C lines can be intricate and time-consuming due to varying exposure and qualitative assessments. Additionally, risk outcomes are not always binary, leading to complex policy wordings and exclusions that may be subject to interpretation during litigation. To address these challenges and bridge the protection gap, insurance leaders are actively exploring technological opportunities. By embracing digital solutions, insurers aim to differentiate themselves and protect their margins beyond just rate adjustments. These investments lead to product innovation, more sophisticated pricing, and improved risk prevention and mitigation strategies. The preferred IT adoption is shifting toward cloud native software-as-a-service (SaaS) solutions due to their flexibility, scalability, easy maintenance, security, and seamless collaboration, making them ideal for the insurance industry’s digital transformation. This involves collaboration between line-of-business (LOB) professionals and IT experts to find effective solutions that drive performance growth, reduce operational inefficiencies, expedite the quoting process, and transform underwriting into a more data-driven and scientific process.

To help navigate global commercial P&C carriers morphing the foundation of the insurance business, this IDC MarketScape assesses IT vendors that provide commercial underwriting workbench applications to help P&C Commercial insurers embrace the following major underlying digital underwriting initiatives:

- Redesign the underwriting value chain. Insurers are seeking flexible, scalable, and compliant underwriting processes to adapt to emerging trends such as direct-to-consumer (D2C) and embedded insurance. IT vendors offer solutions to automate and streamline various stages of the value chain, facilitating collaboration among different stakeholders and reducing resistance to change.

- Employ modern management information frameworks. Insurers require efficient data processing to handle large amounts of information. IT vendors play a vital role in providing technologies that contextualize and analyze data, enabling meaningful insights for underwriting decisions.

- Blend human judgment with data-driven analytics. To cater to the evolving insurance landscape, insurers are embracing a balance between human expertise and data-driven analytics. IT vendors provide tools that empower underwriters with data-driven insights, offering digital upskilling solutions, augmentation tools, and tailored technology selection.

- Adopt an open architecture for prevention-first underwriting. Insurers are collaborating with external partners to offer specialized risk mitigation services. IT vendors assist insurers in adopting open architecture solutions, enabling seamless integration with core and front-office systems, thereby enhancing flexibility and personalized underwriting models.

Through this report, insurers gain valuable insights into the offerings of IT vendors, enabling them to make informed choices and successfully respond to industry changes by adopting more modern tools and workforce approaches to enhance their digital underwriting operations. By encouraging collaboration and knowledge sharing, the IDC MarketScape serves as an authoritative guide for navigating the digital transformation wave in commercial P&C insurance.

From a research perspective in the intelligent underwriting workbench space, the key findings are:

- Comprehensive capabilities. In the competitive landscape of midsize and large commercial line insurers and managing general agents (MGAs), the intelligent underwriting workbench plays a crucial role in streamlining processes and enhancing decision making. The research underscores the importance of comprehensive capabilities within the solution. This includes automated risk rule management, collaborative tools for underwriters, and innovative features that improve efficiency and accuracy throughout the underwriting process. Insurers should prioritize a solution that covers the essential aspects of intelligent underwriting.

- Scalability and customization. The scalability of the underwriting workbench is a significant consideration, especially for growing insurance companies. The research highlights the need for a flexible solution that can adapt to evolving business requirements and accommodate increasing data volumes without compromising performance. Moreover, customization options are essential to tailor the workbench to the insurer’s specific needs, aligning it with unique underwriting processes and company objectives.

- Integration and global compliance. Seamless integration capabilities are key to creating a cohesive digital ecosystem within the insurance organization. The research points out that insurers should seek an underwriting workbench that integrates with existing systems, enabling data flow and process synchronization. Additionally, global compliance is a non-negotiable aspect, especially for insurers operating internationally. The chosen solution should adhere to regulatory standards in multiple regions, reducing compliance-related risks.

- Security measures. Cybersecurity is a paramount concern in the digital age, and the research emphasizes the significance of robust security measures in the intelligent underwriting workbench. Insurers must prioritize data protection, preventing unauthorized access to sensitive information and safeguarding customer data from potential breaches. A comprehensive security framework ensures the confidence of clients and business partners in the insurer’s operations. ▪ Industry expertise and experience. The credibility of the vendor is a vital aspect of selecting an intelligent underwriting workbench. The research highlights the importance of partnering with vendors possessing deep industry expertise and a proven track record in implementing successful underwriting solutions. Such vendors understand the nuances of the insurance sector, offering tailored solutions that align with the insurer’s specific needs and challenges.

- Balance maturity with innovation. Striking a balance between mature, stable solutions and innovative capabilities is a central theme in the research. While insurers seek cutting-edge features to stay ahead of the competition, it is equally crucial to ensure the chosen vendor has a stable foundation and a history of delivering reliable solutions. A well-balanced approach fosters long-term success and adaptability to future industry developments.

- Geographical reach. For insurers with international operations, the geographic reach of the vendor is a critical consideration. The research advises insurers to assess whether the chosen vendor can effectively support their underwriting needs across different regions. A vendor with global presence and an understanding of diverse regulatory environments can better cater to insurers’ multinational requirements.

- User-friendly interface and support capacity. A user-friendly interface is vital for the successful adoption and efficient training of underwriters. The research underscores the significance of selecting an underwriting workbench with an intuitive interface that promotes ease of use and minimizes the learning curve. Additionally, insurers should evaluate the vendor’s implementation and support capacity, ensuring they can deliver timely assistance and guidance throughout the entire deployment process and beyond.

IDC MARKETSCAPE VENDOR INCLUSION CRITERIA

For this IDC MarketScape, IDC Financial Insights will include vendors that have solution offerings aimed at the commercial P&C insurance industry. To be considered in this report, vendors should meet the following criteria:

- The workbench solution should be designed either as standalone or modular so that it can be deployed by itself and not only as part of a product bundle (e.g., policy administration software). As such, the solution should be easy to integrate with legacy systems, solutions from other ISVs, and external service providers (e.g., ecosystem data).

- The solution needs to be commercial off-the-shelf (COTS) software. The solution should provide a highly scalable solution using the latest technology, with little or no customization required for the solution to be suitable for P&C commercial underwriting activities (from point of-sale to coverage approval).

- For the vendor to be included, it needs to demonstrate it offers purpose-built software solutions that integrate at least five out of the following eight modern software underwriting functionalities:

- Advanced artificial Intelligence (AI), automation, and data processing toolsets

- Underwriting decisioning support

- Task management workflow designer

- Persona-oriented user experience

- Full API library

- Full audit and compliance control

- Integrating rating solution

- Low-code microservices architecture

- Given the major advances in technology, solutions that have not received major functional upgrades or redesign cycles since 2017 will be excluded. Solutions should be built using modern design architectures such as microservices, cloud-enabled, modular, and APIs.

- Participating vendors must be present in at least one of the world regions (EMEA, North America, Latin America, Asia/Pacific) and have plans to expand into another one. IDC identified the following companies as meeting these criteria: Salesforce, Appian, Majesco, Insurity, Send, Artificial Labs, Intellect Design, Guidewire, and AdvantageGo.

ADVICE FOR TECHNOLOGY BUYERS

IDC strongly recommends commercial P&C Carriers to embrace intelligent workbench applications to gain a competitive edge. These applications streamline workflows, enhance decision making, and optimize operational efficiency. By leveraging advanced technologies such as AI, machine learning, and data analytics, carriers can expedite quote processing, mitigate risks, and offer personalized services, ensuring a sustainable and future-ready business model. Based on this IDC MarketScape, the vendors assessed in this research offer solutions tailored to the needs of commercial insurers in managing their underwriting activities. To make the right choice and find an ideal underwriting workbench application, insurance technology buyers should consider factors that align with their unique requirements.

- Geographic coverage. Evaluate the geographic coverage offered by vendors. Consider factors such as their global presence, expertise in dealing with local regulations and languages, and ability to cater to specific regional requirements. Choosing a vendor with the right geographic reach ensures seamless operations in the locations where your commercial P&C insurance business operates.

- Business models and portfolio coverage. Understand the business models of vendors and their portfolio coverage. Some vendors may focus solely on underwriting solutions, while others offer a broader range of insurance-related activities. Assess whether your organization requires a specialized underwriting provider or prefers a vendor supporting multiple business needs based on your core commercial insurance operations and procurement strategy.

- Application deployment and cloud. Consider the application deployment options provided by vendors. Evaluate whether your organization prefers on-premises deployment, private or public cloud solutions, or a SaaS model. Ensure the chosen deployment option complies with your insurance company’s ICT governance policies and regulatory requirements.

- Technological innovation and automation. Look for vendors that have adopted modern architectures and innovative technologies to enhance automation in the underwriting process. Features such as optical character recognition (OCR), advanced analytics, and AI can significantly improve underwriting efficiency and accuracy, helping your organization make more informed decisions.

- Learning portals and user community. Examine the user-friendliness of learning portals offered by vendors. These portals should provide centralized access to educational content such as training courses, videos, and articles, creating a learning environment in which employees can share knowledge and best practices. Additionally, consider how vendors engage with their user communities and whether they offer peer-to-peer user communities for collaboration and knowledge sharing, which can enrich your underwriting operations.

- Vendor reputation and customer support. Investigate the reputation and track record of the vendors in the industry. Seek feedback from current customers to assess the quality of their support and responsiveness to issues. A reliable vendor with excellent customer support ensures a smooth implementation process and ongoing assistance, maximizing the value derived from the intelligent workbench application.

- Data security and privacy compliance. Prioritize data security and compliance with privacy regulations when evaluating vendors. Ensure the intelligent workbench application adheres to industry standards and follows robust security protocols to safeguard sensitive customer and company data. Compliance with data protection regulations is essential to maintain trust and avoid potential legal risks.

- Scalability and integration capabilities. Consider the scalability of the application and its ability to accommodate future business growth. An application that can scale with your organization’s needs ensures long-term viability. Additionally, assess the application’s integration capabilities with existing systems and third-party tools to ensure seamless data flow and process automation.

- Cost and ROI analysis. Perform a comprehensive cost-benefit analysis to understand the total cost of ownership and expected return on investment of the intelligent workbench application. Consider factors such as upfront expenses, ongoing maintenance, and potential revenue growth. A clear understanding of costs and benefits aids in making an informed and financially sound decision.

VENDOR SUMMARY PROFILES

This section briefly explains IDC’s key observations resulting in a vendor’s position in the IDC MarketScape. While every vendor is evaluated against each of the criteria outlined in the Appendix, the description here provides a summary of each vendor’s strengths and opportunities.

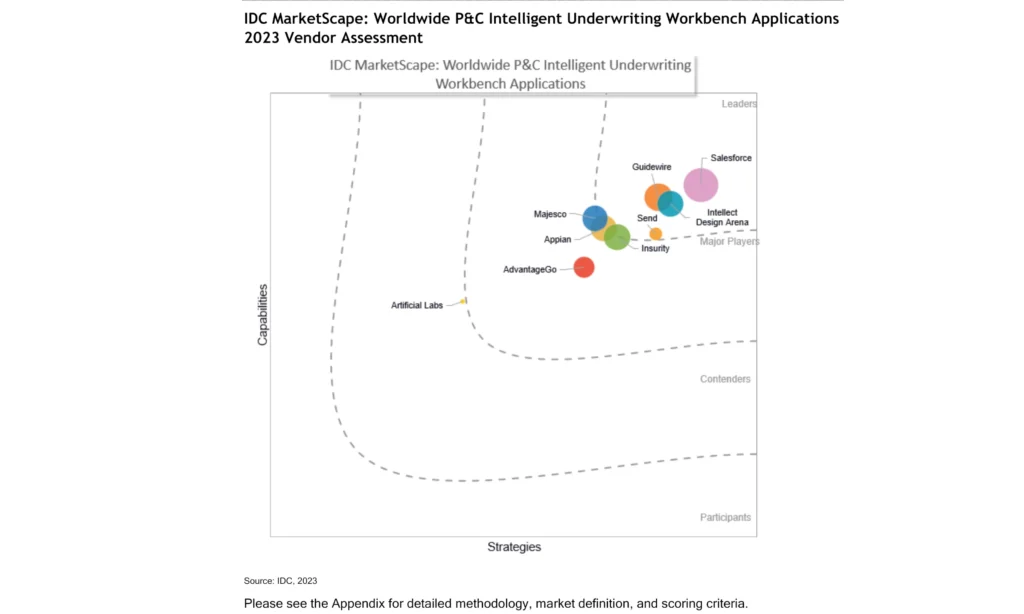

Salesforce

Salesforce is positioned in the Leaders category in this 2023 IDC MarketScape on Worldwide P&C Intelligent Underwriting Workbench Applications vendor assessment.

Salesforce claims a strong global presence with active operations in the U.K. and Ireland (UKI), Europe, the Middle East and Africa, the Americas, Latin America, Asia/Pacific, and Japan. Its global headquarters is in San Francisco, California, U.S. It offers direct in-region and on-demand support across all five major regions, along with partner support in major countries. The company is known for its strong corporate culture, which is based on its core values of trust, customer success, innovation, equality, and sustainability.

Salesforce operates on a predominantly subscription-based business model, offering discounts when applicable. It provides implementation services and multiple levels of support, prioritizing personalized assistance without outsourcing customer support. Its ecosystem strategy revolves around strategic partnerships that foster continuous innovation to enrich the user experience, a value that is reflected in its marketing messaging. The product under assessment is Salesforce’s Underwriter Workbench. Salesforce’s Underwriter Workbench runs on the Salesforce cloud-native platform and offers comprehensive functionality for automating and streamlining commercial P&C insurers’ underwriting processes. Built on Salesforce’s Financial Services Cloud, it acts as a centralized system for managing tasks such as risk assessment, policy issuance, and renewal. Leveraging data and analytics, the solution empowers insurers with informed decision-making capabilities. The Salesforce Underwriter Workbench is also a core component of the company’s Automated Underwriting proposition that enables insurers to extend real-time quote-to-bind and automated submission capabilities to broker partners.

Key features include automated workflow management, intelligent data capture, and real-time analytics. Insurers can optimize operational efficiency and reduce manual effort. The mobile application provides on-the-go access for underwriters, enhancing productivity. Salesforce’s Underwriter Workbench integrates seamlessly with other Salesforce products and functionalities, such as policy admin, claims, billing, and CRM analytics. It also supports integration with external systems, enabling data consolidation and matched insights through Salesforce’s Data Cloud. Security and compliance are prioritized, with role-based access controls and audit trails ensuring data protection and regulatory compliance. Powerful workflow and process management capabilities, powered by Salesforce’s OmniScript, enable the creation of complex workflows and process flows. Task completion is simplified, ensuring consistency and operational efficiency. The Underwriter Workbench provides personalized user interfaces, tailored task lists, and data enrichment options to enhance user experience and enable more efficient decision making. It excels in integration and connectivity through its strong API connectivity, real-time integration capabilities, and with MuleSoft (a Salesforce company). Insurance product configuration, quoting, and policy administration functionality can also be accessed through the Underwriter Workbench. These capabilities are delivered through Salesforce’s Digital Insurance Platform applications that were originally developed by Vlocity, which was acquired by Salesforce in 2020. These now all run natively on Financial Services Cloud.

Salesforce’s Underwriter Workbench runs on Financial Services Cloud and makes use of other Salesforce Cloud capabilities, all built on the Salesforce Platform. To maintain integration and coherence, Salesforce services are typically deployed as blocks of microservices rather than being containerized in isolation. Salesforce provides a comprehensive set of integration solutions, leveraging tools such as MuleSoft, Salesforce Connect, and Integration procedures for seamless data mappingand connectivity. Deployment on Hyperforce infrastructure enables Salesforce instances on public clouds with AWS currently available. Its technology strategy involves close collaboration with customers and partners through advisory councils, market research studies, and a “voice of the customer” program, driving innovation and informing product development. Salesforce’s focus includes deepening functionality, expanding integrations, supporting local integration needs, and enhancing automation and analytics capabilities. Through continued investment in Financial Services Cloud features, process automation, low-code tooling, insurance-specific functionality, data management, integration, analytics and AI capabilities, as well as integrations with partner products, Salesforce aims to meet customers’ specific solution and insight needs in the commercial lines space. These investments and initiatives showcase the company’s commitment to innovation and customer value.

Salesforce Strengths

- Comprehensive insurance capabilities. Salesforce offers an impressive array of features and integrations tailored specifically for insurers. Three automatic releases annually keep it aligned with industry demands, seamlessly connecting with Salesforce’s Policy Admin, Claims, Billing, CRM Analytics, and more.

- Scalable and global. Built on the Salesforce Platform, its Underwriter Workbench easily scales for organizations of all sizes and geographies. Hyperforce infrastructure ensures compliance and enables local data storage, meeting regulatory and data sovereignty requirements worldwide.

- Customizable and low code. Insurance companies can customize the Underwriter Workbench effortlessly using Salesforce’s low-code platform. Simple configuration, no-code/low-code tools, and rule management empower users to adapt processes, build product catalogs, and tailor workflows without extensive programming knowledge.

- Integrated and connected. Salesforce excels in API connectivity and real-time integration. Its Underwriter Workbench seamlessly integrates with external systems, supported by prebuilt connections, integration procedures, and MuleSoft tools. It harmonizes with existing policy administration systems and external rating engines, leveraging insurers’ infrastructure effectively.

Salesforce Challenges

- Pricing complexity. Salesforce’s subscription-based pricing model is occasionally perceived as lacking complete clarity in terms of its alignment with metrics such as user seats and gross written premium. This can lead to confusion among users, particularly small and budget constrained insurance organizations, as they try to understand the correlation between pricing rationale and product usage.

- Inconsistent alignment between Salesforce customers and partners. In some cases in which customers work closely with a Salesforce implementation partner, users may feel a disconnect with Salesforce resulting in possibly missing out on updates, new features, training materials, best practices, and community-driven knowledge sharing.

- Lack of features for more specialized commercial programs. Salesforce, while highly customizable, may have limitations in meeting the unique requirements of advanced commercial programs. Insurance companies may need to invest in additional development, customizations, and integrations to address higher complexity commercial underwriting needs.

Consider Salesforce When

Midsize and large commercial line insurers and MGAs should consider Salesforce when they seek comprehensive insurance capabilities, scalability, customization, integration, and global compliance to enhance their operations and meet industry demands.

APPENDIX

Reading an IDC MarketScape Graph

For the purposes of this analysis, IDC divided potential key measures for success into two primary categories: capabilities and strategies.

Positioning on the y-axis reflects the vendor’s current capabilities and menu of services and how well aligned the vendor is to customer needs. The capabilities category focuses on the capabilities of the company and product today, here and now. Under this category, IDC analysts will look at how well a vendor is building/delivering capabilities that enable it to execute its chosen strategy in the market.

Positioning on the x-axis or strategies axis indicates how well the vendor’s future strategy aligns with what customers will require in three to five years. The strategies category focuses on high-level decisions and underlying assumptions about offerings, customer segments, and business and go-to market plans for the next three to five years.

The size of the individual vendor markers in the IDC MarketScape represents the market share of each individual vendor within the specific market segment being assessed.

IDC MarketScape Methodology

IDC MarketScape criteria selection, weightings, and vendor scores represent well-researched IDC judgment about the market and specific vendors. IDC analysts tailor the range of standard characteristics by which vendors are measured through structured discussions, surveys, and interviews with market leaders, participants, and end users. Market weightings are based on user interviews, buyer surveys, and the input of IDC experts in each market. IDC analysts base individual vendor scores — and ultimately vendor positions on the IDC MarketScape — on detailed surveys and interviews with the vendors, publicly available information, and end-user experiences in an effort to provide an accurate and consistent assessment of each vendor’s characteristics, behavior, and capability.

The adopted IDC methodology is well-structured and looks at multiple dimensions to quantitatively and qualitatively evaluate all involved players to define their vendor positions in the IDC MarketScape. This is an intensive exercise that entails several steps, including desk research, defining a comprehensive request for information for the vendors, in-depth interviews and demos with vendors, and interviews with vendors’ customers. This methodology enables IDC to combine all information and complement them with customers’ experiences and perceptions, thereby an IDC MarketScape leverages multiple perspectives that contribute to the final evaluation that is based on a standardized set of parameters.

This IDC MarketScape on Worldwide P&C Intelligent Underwriting Workbench Applications presents a 2022-2023 assessment of solutions that vendors offer to address trade finance. Please note that not all information used in the evaluation process is public knowledge, particularly when it comes to forward-looking strategies. IDC appreciates participants’ trust to share confidential information to enable a comprehensive and detailed assessment that is corroborated by customer references. As trade finance technology is evolving quickly, IDC invites all readers to pay attention to market developments as there are major announcements anticipated in the near future.

Collaborating in an IDC MarketScape assessment is quite a commitment, and IDC thanks all participants from Salesforce, Appian, Insurity, Majesco, Intellect Design, and Send for their support and involvement. Unfortunately, Guidewire and Artificial Labs decided not to actively participate in the process. Nevertheless, IDC included both since they are application-relevant vendors in the ecosystem, and their evaluations are based on publicly available information, customer references, and existing knowledge of their solutions.

Market Definition

The underwriting process is a critical and fundamental component within the insurance value chain. It entails the thorough evaluation of risks associated with an insurance policy, the appropriate pricing of the policy, and the ultimate decision of whether to accept or reject the risk. However, the traditional underwriting process has long been plagued by manual, paper-based practices, heavily reliant on subjective judgment. This outdated approach can be time-consuming and prone to errors, leading to inconsistent risk assessments, inaccurate policy pricing, and slow turnaround times.

Over the past few years, the insurance industry has been witnessing a significant trend toward digitization and automation of underwriting and policy administration processes. Nowhere is this trend more prominent than in the commercial property and casualty (P&C) lines, in which the underwriting process can be intricate and time-consuming. In this context, the adoption of underwriting workbench solutions has been gaining traction. These solutions are purpose-built software applications designed to streamline processes and analyses for commercial P&C insurers of all sizes, providing a comprehensive one-stop-shop environment. Augmented with features such as artificial intelligence (AI), machine learning (ML), and automatic data gathering and processing, these solutions greatly enhance commercial underwriters’ capabilities. IDC Financial Insights conducted an IDC MarketScape assessment, evaluating various commercial P&C underwriting workbench solutions. The assessment revealed that an underwriting workbench can be defined as a single pane of glass, seamlessly integrating with existing technology, and offering a unified user experience across multiple devices. This integration empowers underwriters to effectively manage new businesses, renewals, and endorsements, improving efficiency and reducing operational complexities. Insurers globally stand to benefit significantly from such cutting-edge and cooperative features, including greater organizational agility, increased underwriter capacity, and heightened levels of customer and employee/intermediary satisfaction, thanks to modern and self-service capabilities.

The adoption of underwriting workbench solutions can lead to transformative outcomes for insurance organizations. Improved underwriting profitability, enhanced operational efficiency, better risk management, and elevated customer experience are some of the key advantages. By embracing these solutions, insurance companies can stay ahead of the competition, optimize their bottom lines, and provide superior service to their customers, thereby achieving sustained success in the dynamic and ever-changing insurance market. The move toward digitization and automation represents a pivotal step for insurance organizations, as they adapt to the demands of the modern era and enhance their competitiveness in the industry.