Throughout the financial services industry, customers are looking for more personalized, streamlined and convenient experiences without compromising on trust and security. The insurance industry has already made strides to adapt to these trends by seeking out ways to automate operations and use artificial intelligence (AI) to generate insights and predict trends in a bid to become more agile and responsive as an organization as well as in responding to customer needs.

In June and July of 2023, Arizent and Digital Insurance surveyed 105 respondents holding manager-level positions or higher at insurance carriers, agencies and brokerages. The research, done on behalf of Salesforce, suggests insurers see substantial additional opportunities to leverage automation and AI within their operations, provided they can overcome key challenges such as privacy, security and implementation issues.

Predictive vs. Generative AI

The key difference between the new generation of AI and previous generations is the ability to create something new. Predictive AI is already capable of looking at a broad set of data and drawing out key insights, such as customers who are ripe for upselling opportunities or policies written in high-risk areas. Generative AI can collect these insights and turn them into useful information, from a comprehensive set of pre-meeting notes to a set of personalized tips on how policyholders in high-risk areas might stormproof their homes. This ability to create new content, including drafting emails and scheduling meetings, frees up more time for producers to attend to higher-value tasks while also maintaining a high level of customer support and engagement

With Salesforce + AI, Insurers See Improved Efficiency and engagement

Data has long been the lifeblood of the insurance industry. For more than 100 years, insurers have relied on data to price their policies and manage risk. Modern technology offers more ways to analyze and leverage that information than ever before. Combining data with modern automation and workflow technology is giving the insurance industry an opportunity to reimagine the way organizations operate while also creating personalized experiences, making the business more efficient and predicting adverse events more accurately.

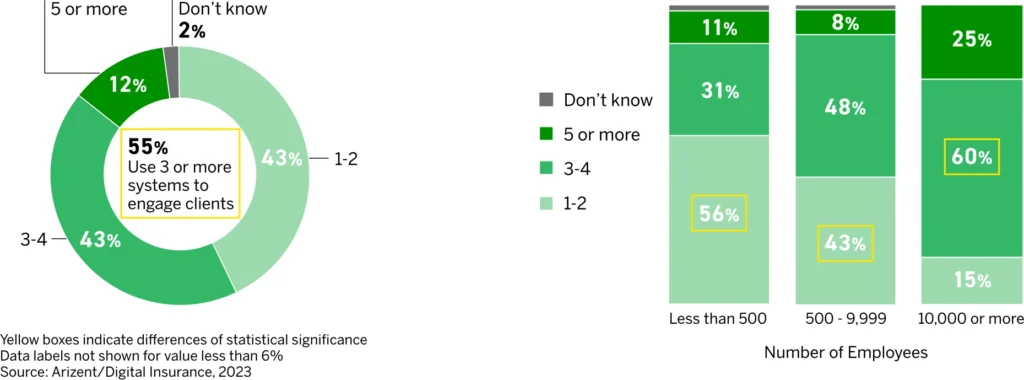

With these potential benefits in play, a majority of insurers are actively adopting new technology tools to improve various elements of their operations. In many cases, they are not hesitant to deploy these tools: 60% consider themselves early majority adopters of new technology. Still, some areas remain a substantial challenge. Entering and updating customer data still consumes a lot of organizational resources. Carriers also spend a lot of time fielding inbound customer support calls. These inefficiencies stem in large part from the cumbersome set of technologies in use to manage the insurance sales process. More than half of respondents report using three or more different technology systems as they work from initial engagement to the close of a sale (see Figure 1). This challenge becomes even more evident in larger organizations with broader product offerings

Insurance Firms Use 3+ Systems to Engage Customers

With insurance firms using three or more systems for client engagement, the potential for key data or potential cross-sell opportunities could easily be getting lost in the shuffle if the systems aren’t connected in a way that offers brokerages and agencies a 360-degree view of their policyholders.

AI + Salesforce Technology Yields ROI

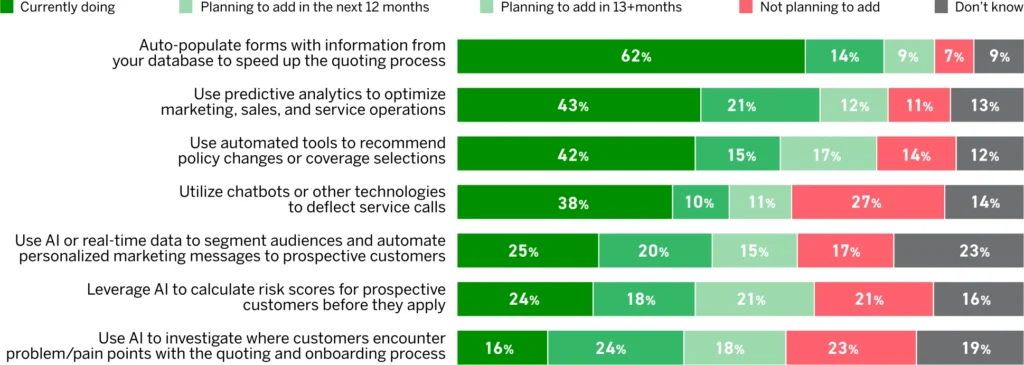

Automation technology is playing a key role in making insurers’ workflows more efficient. Auto-populating forms that speed up quoting are in use at 62% of firms. Technology that aids with data analysis, including artificial intelligence (AI) tools, are also becoming more common as insurers seek to personalize policies across every potential decision point in a policyholder’s lifecycle. Roughly four in 10 insurers (43%) use predictive analytics to optimize marketing, sales and service operations. A similar number (42%) use automated tools to recommend policy changes or coverage selections. And 38% use chatbots or other technology to deflect service calls.

AI Technology is Used to Streamline Customer Journeys

Insurers are also leveraging AI to support a variety of business processes across the front, middle and back office. For example, 37% are using AI to help identify ways they can reduce underwriting risk and improve profitability. Three in 10 are monitoring agent performance in search of ways to improve productivity and provide personalized marketing to engage customers more effectively. Roughly the same number (29%) are using AI to glean insights that make the claims process faster and reduce its susceptibility to fraud.

Onboarding and personalization are two key areas of focus for these efforts. Nearly half of firms (49%) are currently using real-time data to target customers for cross-sell or upsell offers or to personalize and speed up the onboarding process. A substantial number of insurers plan to add these capabilities in the coming years as well. The use of AI can help turn this analysis into insight quickly, for example by predicting disruptions and alerting brokers before they start hearing directly from claimants. With these types of tools, insurers can take advantage of opportunities to get the right offer to the right customer at the right time.

Insurers Face Challenges to AI Adoption

Despite the variety of areas in which AI can help insurers, fully 25% say they aren’t using it at all yet. Even those who make use of it in some areas find it at least moderately challenging for one reason or another. The most common challenges include a lack of talent (79%) or vendors (70%) to implement the AI solutions that would meet insurers’ needs. Privacy, security and compliance concerns involved with the use of AI also create challenges for 75% of respondents. In other cases, insurers lack the technological underpinnings necessary to take advantage of AI — 69% say their use of AI is hampered by an inability to get access to the right data in the right format.

Build More Intelligent Technology

As AI continues to mature, insurers will be able to extend its benefits to more parts of the organization. To lay the groundwork for greater use of AI, insurers must first streamline their operations and focus wherever possible on technology that has secure intelligence capabilities already integrated within it. These technology choices can help reduce the challenges insurers currently face ensuring AI systems conform with privacy, security and compliance requirements.

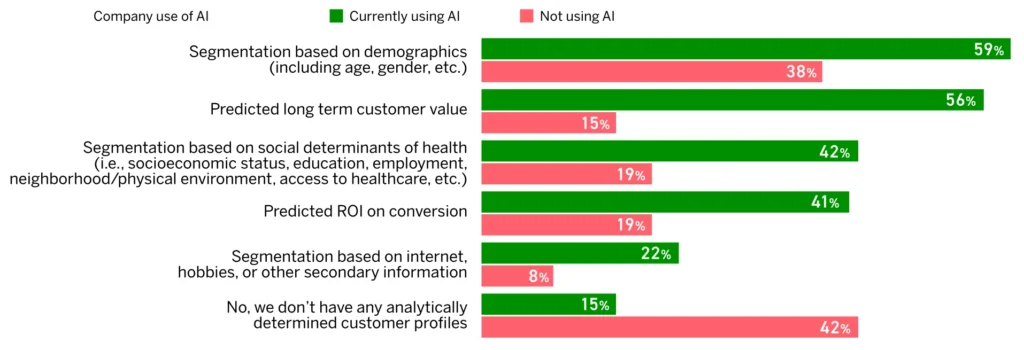

In many cases, insurers are already using some form of predictive intelligence to help agents segment customers in their prospect database and move customers through the sales and service process more quickly. For example, firms can analyze the demographics they serve to get insights about the market segments or premium value groups they serve most effectively, or to identify customer segments they should prioritize for support. Some firms are also leveraging third-party data to identify relationships between prospects and existing customers to prioritize the most promising leads.

AI clearly helps support these efforts. Firms using AI are significantly more likely to be segmenting customer populations based on their relative benefit to the business, including their predicted long-term customer value, demographics, social determinants of health and predicted ROI on conversion.

Insurance Can Use AI to Leverage Customer Segmentation

To make their tools easier to implement and more effective for the business, insurers can work to reduce the number of systems they need to achieve a more intelligent sales and service process by using a customer relationship management (CRM) system capable of applying intelligence to the data it holds. Because a CRM system is generally the first to become populated with data about a prospect, it makes sense as a central repository of information as those prospects convert to customers and as relationships with those customers deepen. CRM solutions that can apply intelligence to that information solve for the challenge of getting the right information to the right system at the right time. They also simplify privacy, security and compliance oversight, since it’s only necessary to implement a set of restrictions once in a single system, rather than tracking sensitive information across multiple systems throughout the enterprise.

Prepare for A More Intelligent Future

The types of benefits data intelligence can provide continue to advance. The rise of generative AI provides a new set of benefits by presenting this intelligence in a more efficient and actionable package (see “Predictive vs. Generative AI”). Before they can confidently take advantage of these opportunities, however, firms will need to pilot them and roll them out more broadly within the organization. This process will enable them to work out any potential issues before they apply them to client-facing processes and ensure internal systems are properly equipped to use these tools appropriately.

For example, integrated technologies can make it possible to use intelligence on internal-facing systems first, ensuring a human remains in the loop to guide decision-making. This type of process can also help maintain human review as insurers roll out intelligence-aided client-facing recommendations. This degree of oversight can help tune AI and machine learning models to an organization’s specific needs. In the case of generative AI, it can also help organizations develop well-crafted prompts that yield their desired results.

In the near term, generative AI systems will help improve efficiency by helping insurers process information and make recommendations. Currently, intelligence generates the information producers use to develop insights on their own. For example, a producer or territory manager prepping for a meeting with an agent can get information on likely-to-leave or renewal models, as well as risk performance. They can then use that information to gameplan for a meeting with the agent. Using generative AI, the same producer or territory manager can craft a prompt that the intelligence engine can use to produce a document that collates and highlights all of this information for them, along with a set of recommended next best actions. Additionally, the intelligence engine could produce a customized email recommending a mutually workable meeting time that the producer could quickly tweak as needed before sending along to the agent.

As helpful as this technology can be, it also requires ongoing governance to detect and manage unintended consequences. Partners who understand this technology and how it works with your data are critical for getting this right.

A CRM capable of producing real-time data throughout a workflow can act like a digital backbone for an organization. With access to behavioral data and generative AI, producers will simply need to ask the right questions to generate insights and materials that save them time and produce a better customer experience.